What Entrepreneurs Should Know About S-Corps

Some of the most frequent tax questions entrepreneurs have are about S-Corps. For freelancers and many small businesses, S-Corps can be great. But for many startups, they can cause lots of problems.

This post is full of a ton of information to help you decide if an S-Corp is right for you. It’s divided into three parts:

- What’s S-Corp

- When S-Corps are good; when S-Corps are bad

- How to reduce your taxes using an S-Corp

1. What is an S-Corp

Some History

Historically, entrepreneurs only had two options to form a business entity (we will ignore LLCs for a moment, which are only a few decades old):

(1) Form a general partnership and (a) benefit from a reduced tax bill due to “pass-through” taxation, but (b) be subject to full personal liability for all business debts and liabilities; or

(2) Form a corporation and (a) benefit from limited personal liability for the business’ debts and liabilities; but (b) be subject to a higher tax bill due to “double-taxation.”

Neither option is fully ideal. One will result in more income but higher risk, the other will result less risk but lower income. In the 1950s President Eisenhower led the charge to make a middle option: allow a corporation to “pass through” its income while still benefiting from the limited liability associated with corporations. And in 1958, Congress agreed and enacted Subchapter S of the IRS Code. As a result, business owners can form a corporation and make an S-Corp election and receive a lower tax bill and limited liability.

But here’s something important to remember – an S-Corp is not a business entity.

When you form your business entity with your Secretary of State, you can choose partnership, limited liability company, corporation, or non-profit corporation. But you cannot choose “S-Corp.” That’s because it is merely a tax classification.

S-Corp Restrictions

It is very important to note that there are specific requirements you must meet if you want to take advantage of S-Cop taxation. And they are not ideal for many businesses, especially high-growth potential startups that want to raise venture capital.

According to the IRS, to qualify for S-Corporation status today a corporation must:

- Be a domestic corporation

- Have only allowable shareholders

- May be individuals, certain trusts, and estates and

- May not be partnerships, corporations or non-resident alien shareholders

- Have no more than 100 shareholders

- Have only one class of stock

- Not be an ineligible corporation (i.e. certain financial institutions, insurance companies, and domestic international sales corporations).

The Lawyer's Guide to Entrepreneurship

2. When S-Corps are Good; When S-Corps are Bad

When S-Corps May be Good

The two types of businesses most likely to benefit from an S-Corp election are

(1) Freelancers who operate using an LLC or Corporation and make more than a “reasonable” salary for their given profession; and

(2) Small businesses owned by individuals (as opposed to other business entities) with small and simple legal structures.

These kinds of businesses probably meet the requirements to be an S-Corp (see above) and are unlikely to change their business structure in the future. That’s important because if you make a change to your business and fail to meet the requirements, you’ll lose your S-Corp status and may suffer serious financial consequences as a result.

After making the S-Corp election, these business will gain two primary benefits: (i) They can avoid paying corporate taxes on the businesses income and instead, “pass through” all the income to the owners’ individual tax returns; and (ii) they can reduce their tax bill by treating part of their income as profit distributions (see below).

When S-Corps May be Bad

Sometimes it can be a really bad idea to make an S-corp election.

Specifically, many businesses don’t meet the requirements (see above) (for example, they are owned by an ineligible owner, have multiple ownership classes, etc.). In those scenarios, it is pretty obvious that they shouldn’t make an S-Corp election.

In another example, you may meet the requirements, but it still might mot make sense to make the election. This is especially true for high-growth potential startups that need to raise money from investors. That’s because an S-Corp can only have 100 owners (which means you can’t go public), it can’t be owned by most types of business entities (which means many investors can’t invest in the company), and it can’t have more than one classification of ownership interest (which means you can’t grant preferred stock to your investors).

(For clarity, you can always revoke (or accidentally bust) your S-Corp election to get out from the restrictions, but doing so usually results in severe, and negative, financial consequences.)

3. How to reduce your taxes using an S-Corp

The Default 15.3%

When you earn money, the IRS expects to collect 15.3% for Social Security and Medicare (in addition to other business and individual taxes).

If you are employed, you’ll pay 7.65% and your employer will pay the other 7.65%. However, if you are self-employed, you have to pay the entire 15.3% yourself. This is true for Sole Proprietors and also partners in a Partnership (and also true for LLC owners if the LLC is taxed as a Sole Proprietorship or Partnership). (There are some limits to this, plus you’ll pay various income taxes and other taxes. But we’re trying to keep things simple here.)

The S-Corp Exception

When you elect to be taxed as an S-Corp, the IRS will collect that 15.3% on your salary, but you can pass your profits through to your personal tax return without paying that 15.3% on those profits. That’s where the savings comes in. 15.3% of your profits can add up to a significant savings in some situations.

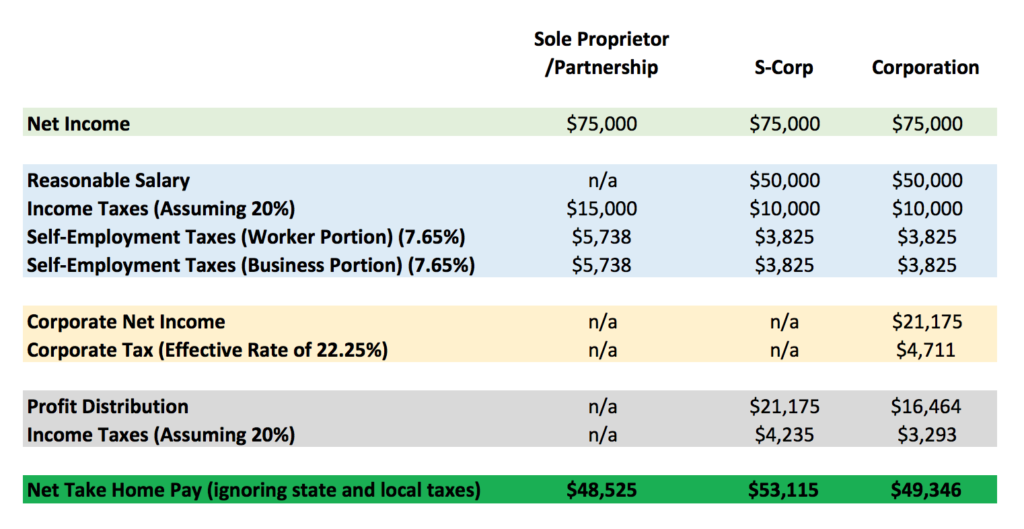

A Practical Example

In the example below, we show what federal taxes you’ll owe based on $75,000 in net income. This example assumes your individual tax rate is 20% and that your effective corporate rate is 22.25%. It also ignores state and local taxes. (Seriously, this is an overly simple example, but we’re trying to get to the heart of the benefits of S-Corps.)

As you can see, your tax classification will impact how much money you take home at the end of the year.

Being taxed as a Sole Proprietor is the easiest, but not the most profitable. Paying taxes as a Corporation looks better, but in the real world it is more expensive to operate as a Corporation so you won’t really see a savings there (corporate formalities, additional state-level taxes, extra tax return filings, etc.).

However, right in the middle you’ll see how the S-Corp election can save you money. You can avoid corporate taxes and avoid the 15.3% self-employment tax on your profits. At the end of the day, at least in this example, your net take home pay will be highest by making an S-Corp election.

What This Means for You

Clearly, making an S-Corp election can result in more money in your pocket at the end of the year. But as we explained above, there are other reasons why you might not want to make the election.

And further, even in this “simple” example, it is all quite complicated. And there is more to it than described above. That’s why you should always talk with an accountant and a lawyer before making any tax classification decisions for your small business, especially if you are a high-growth potential startup.

(This article is general in nature and is not legal advice.)

Free Guide: The Lawyer's Guide to Entrepreneurship

Maximize your success with the right legal foundation.

LLCs v. Corporations

Finances & Taxes

How to Hire

Intellectual Property

Contracts

And More!